After considerable fanfare, the first U.S. regulated bitcoin futures were launched on Sunday, Dec. 10 at the Cboe Futures Exchange (CFE). The inaugural session and initial week of trading went smoothly.

The first full session, which concluded on Monday, Dec. 11, had 4,127 contracts trading. At contract launch, there were three contract expiries for XBTSM futures: January, February and March 2018. Average daily volume (ADV) for XBT futures on week 1 was 2,209 (ADV number is through Thursday.)

Front-Month Futures Dominate

Front-month XBT futures (XBTF8 – January contract) dominated trading volume all week, averaging over 90% of the total futures volume. The preponderance of trade volume in other futures contracts tends also to be in the front-month contract.

Bitcoin spot price fluctuated between $14,765 and $17,920 on the Gemini exchange between the Sunday open for XBT futures and Friday (Dec. 15) at 9:30 a.m. CT when this data was pulled.

The January futures contract traded between $15,000 and $18,850 over the same time frame. The largest intraday range occurred during the first full session. Since then, realized volatility in the cash and futures markets have been relatively muted. However, when addressing bitcoin volatility in 2017, it is arguably always “relative.”

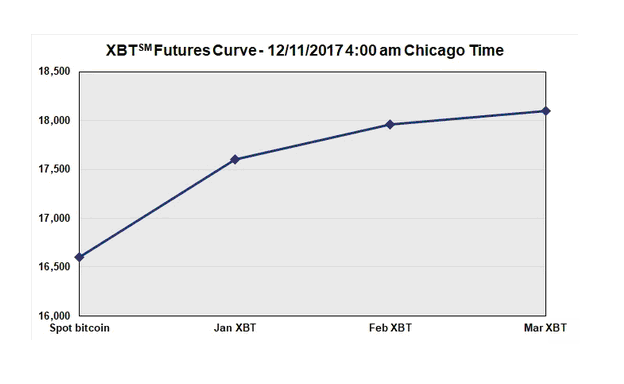

The futures term structure opened in contango and remained that way all week. Contango implies a forward-sloping futures curve with front-month futures trading at a premium to the spot market, and further-dated months trading even higher.

Commodity markets exhibit a “normal” or contango term structure most of the time. An understanding of term structure is important if you are new to futures markets.

The big story of the week is the narrowing of the front month to cash premium as the week progressed. On Sunday evening, January futures opened a slight (2.1%) premium to the Gemini cash market. However, that spread widened considerably in the hours that followed. The cash market moved steadily higher between Sunday afternoon and early Monday morning, but the futures did so with noted velocity. January futures briefly traded at a nearly $2,000 (11.9%) premium to the cash market ($18,850 vs. $16,875).

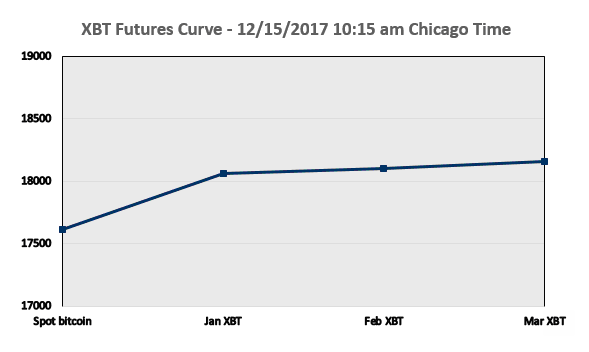

Between midnight Dec. 11 and the early morning of Dec. 14, this premium was largely erased. As you can see from the term structure graph that Russell Rhoads used in his blog about hedging using the XBT futures, the spread had narrowed to about $1,000 (6.0%) by 4 a.m. CT on Monday morning.

At last check (Dec. 15), January was trading at roughly a $450 (2.6%) premium to cash. So, while contango persists, the term structure has flattened a great deal over the course of the first week of trading.

Breakdown of daily #BitcoinFutures volume traded at the Cboe Futures Exchange – volume heavily focused in front month #Bitcoin $XBT @GeminiDotCom https://t.co/hVLJjX5RaY pic.twitter.com/Cpnc2SYFme

— Cboe (@CBOE) December 21, 2017